K-pop built a $4.5 billion superfan economy — and the rest of the world is copying it. Photocards, fansigns, streaming coordination: how devotion became a self-sustaining revenue machine.

that I was here. That he might see me. Yuna, 24 · Seoul · Stray Kids fan · 47 albums purchased this comeback

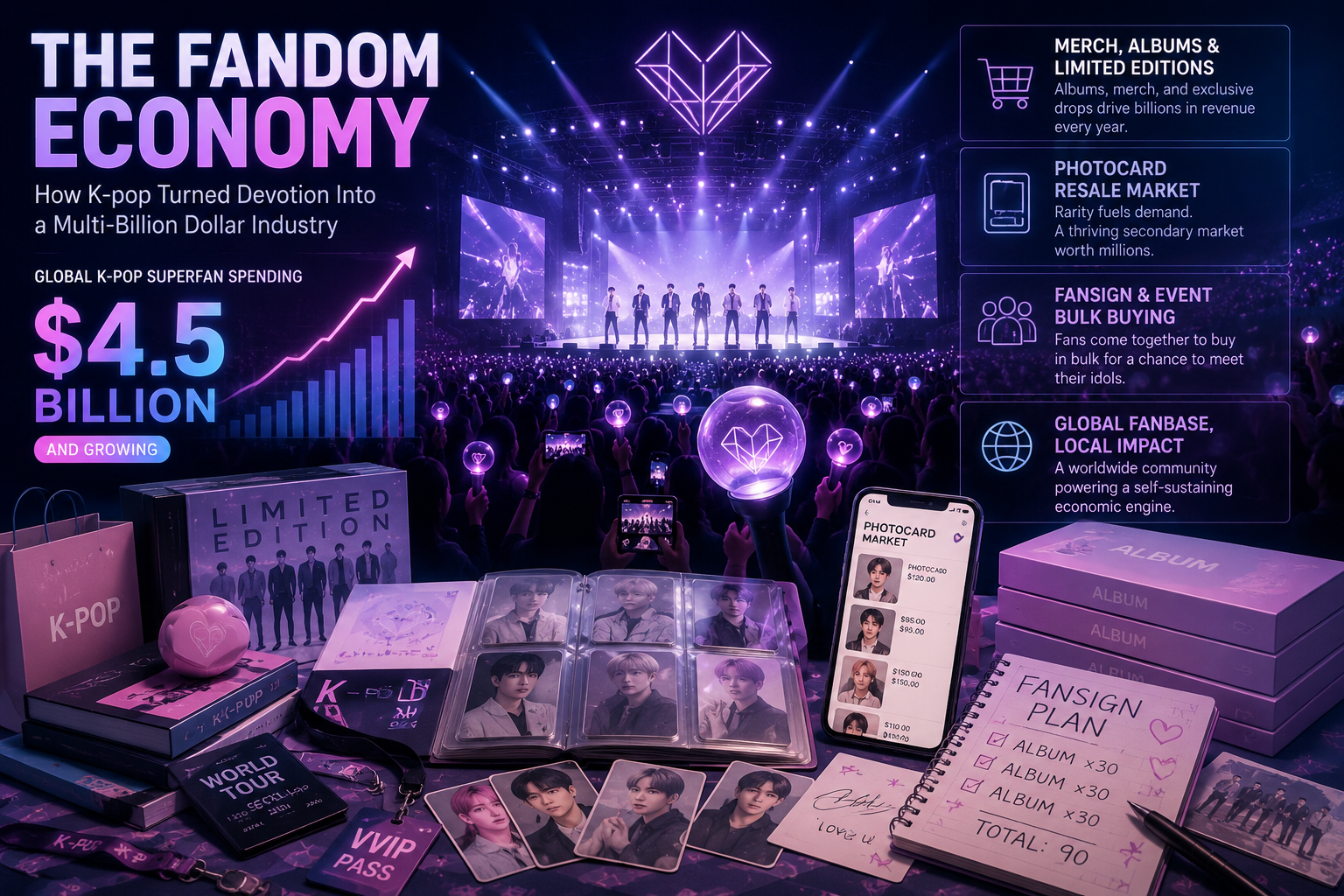

To understand the K-pop fandom economy, you have to start with one number. In its 2023 Music in the Air report, Goldman Sachs identified superfan monetization as an untapped market worth $4.2 billion annually. The following year, the bank revised that figure upward — to $4.5 billion. For context: the entire global recorded music industry generates roughly $30 billion a year. The superfan economy that K-pop invented and perfected is worth, on its own, a sixth of everything traditional music makes. K-pop didn’t just build a genre. It built an economic operating system — and the rest of the world’s music industry is now frantically reverse-engineering it.

The Architecture of Devotion

It is 3:47 a.m. in Bangkok. A graduate student is curled beneath a duvet, scrolling her phone. A notification lights the screen: her favorite idol has sent a message on Bubble — 120 characters about how practice ran late tonight. She pays $8 a month for this. For the possibility that this moment exists.

And that $8 is, by a wide margin, the cheapest line item on her monthly budget.

K-pop fans don’t just consume music. They operate within a layered economic architecture — each floor designed to convert affection into expenditure, and expenditure into deeper affection. Understanding the machine means walking through it from the ground up.

A K-pop album is not primarily a music delivery mechanism. The standard physical release contains a CD, a photobook — and, critically, a photocard: a small, trading-card-sized photograph of one group member, inserted randomly. In a seven-member group, collecting your favorite member’s card means buying, statistically, seven copies. Most albums release in four to six versions, each with its own photocard pool. Fansign entry tickets scale with purchase volume. The math is designed to cascade. SEVENTEEN’s FML — the top-selling physical album of 2023 — was released in six distinct versions. In 2024, 17 of the 20 best-selling albums in the world were by South Korean artists. In a streaming-dominated market, this makes no sense unless you understand that the album-as-object is functioning as something other than music.

The photocard secondary market has become one of the stranger economic phenomena of the decade. Rare cards — promotional exclusives, event-only prints, signed versions — have become legitimate collector’s items with their own grading ecosystem. Third-party grading services like PSA (Professional Sports Authenticator), built for baseball and basketball cards, now formally evaluate K-pop photocards. The global star trading card market is projected to grow from $1.6 billion in 2025 to $3.6 billion by 2032, a compound annual growth rate of 12.4%. On Bunjang, one of Korea’s largest resale platforms, the top photocard transactions in 2025 saw individual cards from Stray Kids and aespa selling for over $1,500 each. Signed albums crossed the $2,000 mark. These are not cautionary tales — they are aspirational data points within the community.

The fansign — a live event granting fans a few minutes with their idols, or in online format a video call lasting under a minute — is K-pop’s most psychologically sophisticated commercial mechanism. Access is distributed by lottery. Entry tickets come with album purchases. For a competitive offline fansign with thousands of applicants, a realistic shot at selection requires dozens of purchases, sometimes hundreds. Fans who don’t win keep the albums. Or they don’t — the streets around major Seoul record stores, and platforms like Daangn Market, are perpetually stocked with K-pop albums whose photocards have been removed and the disc discarded. Korea’s Content and Tourism Institute has explicitly flagged fansign-driven bulk purchasing and the resulting album disposal as a growing systemic concern for the industry.

I spent about $400 trying to get into one fansign. I didn’t get in. But I got every member’s photocard — and I met other fans who were buying with me. We became real friends. Was it worth it?

— Ji-woo, 26, BusanThe Numbers: What Fans Actually Spend

According to Luminate’s 2023 Annual Report, U.S. K-pop fans spend an average of $24 per month on merchandise — 2.4 times higher than the average American music listener, and $8 more monthly than J-pop fans. U.S. K-pop fans are also 50% more likely to purchase merchandise even when they cannot attend a live event. But averages obscure a spending distribution that looks nothing like a bell curve.

| Fan Tier | Primary activity | Est. annual spend |

|---|---|---|

| Casual Listener | Streaming only | $0 – $20 |

| Light Fan | Occasional merch / social follows | $20 – $100 |

| Core Fan | Album preorders, livestream concerts | $100 – $200 |

| Superfan | Photocards, fanmeets, limited merch | $500 – $1,500+ |

Luminate’s 2025 mid-year report defines a superfan as someone who engages through five or more of thirteen possible channels — attending live or virtual concerts, purchasing albums or merchandise, participating in fan communities, subscribing to newsletters, and more. Roughly 20% of all music listeners qualify. Their spending diverges sharply: superfans spend 66% more on live events and more than twice as much on music purchases as typical consumers, with a concert attendance rate of 90% against a general average of 59%.

And the platform layer compounds everything. Supporting a full-member roster through Bubble alone can cost over $30 per month — a figure that excludes Weverse memberships, concert tickets, and physical goods. Some superfans now spend several hundred dollars monthly across multiple platforms.

I track it in a spreadsheet. If I didn’t, I genuinely couldn’t tell you the total. I’m not sure I want to know.

— Hana, 28, Toronto · follows three groupsThe Machine: How Fandom Became the Product

Here is where K-pop diverges fundamentally from every other model in the global music industry. Western music executives have historically treated the song as the product. Korean entertainment conglomerates understood years ago that the song is a marketing funnel — a loss leader, almost. The real product is intimacy itself. And intimacy, structured correctly, generates recurring revenue at software-margin levels.

HYBE’s 2025 financials make the argument more powerfully than any analyst report.

The traditional core product declined while the company broke records. Because the product was never the music. Weverse Shop sold 25.2 million products in 2025 alone, with digital product purchases more than doubling year-over-year. Fans spent an average of 263 minutes per month on the platform. The company staged 279 concerts across 53 cities — up from 172 the prior year. The “Artist-Indirect” business segment, generating revenue without requiring the artists’ active participation, grew 19.3% to approximately $679 million.

Streaming Operations: The Unpaid Marketing Department

Perhaps nothing illustrates the gap between K-pop fandom and conventional music listening more sharply than 총공 (chong-gong) — “total attack.” On the day of a comeback, fan Discord servers and KakaoTalk group chats distribute minute-by-minute schedules: which platform, which hour, how many consecutive streams, which accounts to rotate, whether to use a VPN and to which region.

Fans collectively and voluntarily perform what amounts to coordinated labor — repeating streams of a new release to improve chart positions — without compensation, organizational hierarchy, or coercion. No marketing agency can purchase this behavior.

- Streams music passively

- Buys merchandise at concerts

- Follows artist on social media

- Attends 0–1 shows per year

- ~$10/month avg. spend

- Consumer of the product

- Coordinates streaming campaigns

- Buys multiple album versions for cards

- Subscribes to DM platforms ($8–$30+/mo)

- Attends fan events, fanmeets, concerts

- $500–$1,500+/year avg. spend

- Distribution engine for the product

K-pop companies didn’t create this impulse — it emerged organically from fandom culture. But they recognized it early, and they designed their entire ecosystem to channel it. The album versions, the photocard randomization, the chart certification systems that reward sales velocity, the fansign tickets tied to purchase counts — every mechanism gives fans a concrete, gamified action they can take to help. The fan is not a consumer. The fan is a distribution channel, a marketing engine, and in moments like chart weeks, effectively an investment vehicle for an artist’s commercial future.

The Other Side: Cracks in the Foundation

This story has shadows. The domestic market is softening. Circle Chart’s 2025 mid-year report found total digital music consumption for the top 400 songs had fallen 6.4% year-on-year, and was down nearly 50% from the genre’s 2019 peak. Physical album sales dropped 9%. In 2024, Korean domestic album sales had already fallen 19%, slipping below 100 million units for the first time since the boom began.

Record year for physical sales. K-pop dominates global physical charts. SEVENTEEN’s FML sells 6.2 million units.

Only 20 million-selling albums — down from 33. Top-tier groups see sales roughly halved. Shares in the four major entertainment companies fall ~19% on average.

Solo artists dominate domestic digital charts. Seven of the top 10 in the first half of 2025 are solo performers. Idol group chart dominance fades domestically.

Revenue of $1.86B driven by concerts (+69%) and merchandising (+35.8%), not music. The model has decoupled from album sales.

The most searching critique comes from academia. A 2025 study published in Popular Music and Society applied labor process theory to Bubble’s business model, analyzing how the platform commodifies fan emotional labor. The paper joins a growing body of scholarship questioning whether K-pop fandom’s celebrated “participation” is, in structural terms, distinguishable from work — and if so, whose interests that work ultimately serves.

Am I buying the album, or is the album buying me?

— Yuna, 24, Seoul · 47 albums, one comebackWhat Comes Next

The K-pop fandom economy stands at a pivot point. The big entertainment companies are moving aggressively toward live revenue, international markets, and platform subscription models — building moats that don’t depend on first-week chart numbers.

HYBE’s own trajectory points toward the answer: even as BTS members served their mandatory military service and group activities paused, company revenues continued to climb. The ecosystem was designed to outlast any individual cycle. And now, with BTS’s return — the BTS WORLD TOUR ‘ARIRANG’ spanning 82 shows across 34 cities and 23 countries, the largest stadium world tour in K-pop history — the system is being tested at its highest ceiling yet.

- Superfan TAM$4.5B addressable market per year — Goldman Sachs, 2024 estimate

- US Fan Spend$24/month average on merchandise — 2.4× the general listener (Luminate, 2023)

- Superfan Spend$500–$1,500+ annually for top-tier fans across merch, platforms, and events

- Album Exports$291.8M in international physical K-pop album sales in 2024 (Korea Customs Service)

- Photocard MarketGlobal trading card market: $1.6B in 2025 → $3.6B by 2032 (CAGR 12.4%)

- Platform ReachWeverse: 12M peak MAU · Bubble: 2M+ paid subscribers · Berriz: 202 countries

- HYBE FY2025$1.86B revenue (record) — concerts +69%, merch +35.8%, recorded music –10.2%

Data cross-verified from: HYBE FY2025 Investor Presentation; Goldman Sachs Music in the Air 2023 & 2024 editions; Luminate 2023 Annual Report & 2025 Mid-Year Report; Circle Chart 2025 Mid-Year Report (Korea Herald); Korea Customs Service export statistics; Bunjang 2025 K-pop Merchandise Report; DearU/Bubble corporate filings; Weverse 2025 Fandom Trend Report (HYBE, February 2026); KCTI industry analysis; Global Star Trading Card Market research (2026); Popular Music and Society (2025). Fan spending tier estimates synthesize multiple sources and represent directional ranges, not audited figures. Fan quotes are from interviews conducted for this series; names changed at subjects’ request.