In 2019, HYBE launched Weverse. In 2020, DearU launched Bubble. In March 2025, Kakao Entertainment launched Berriz. In five years, K-pop built a platform economy that the rest of the global music industry is now desperately trying to replicate — and three companies are currently fighting over who gets to own it.

Three Platforms, One War

To understand the K-pop platform wars, you have to understand the prize. K-pop fandom is not passive. Fans don’t just listen — they subscribe, they post, they buy, they show up. The platform that captures this engagement captures something more valuable than a user: it captures a lifestyle, a community, and a recurring wallet. The three major platforms fighting for this market have each chosen a fundamentally different strategy to win it.

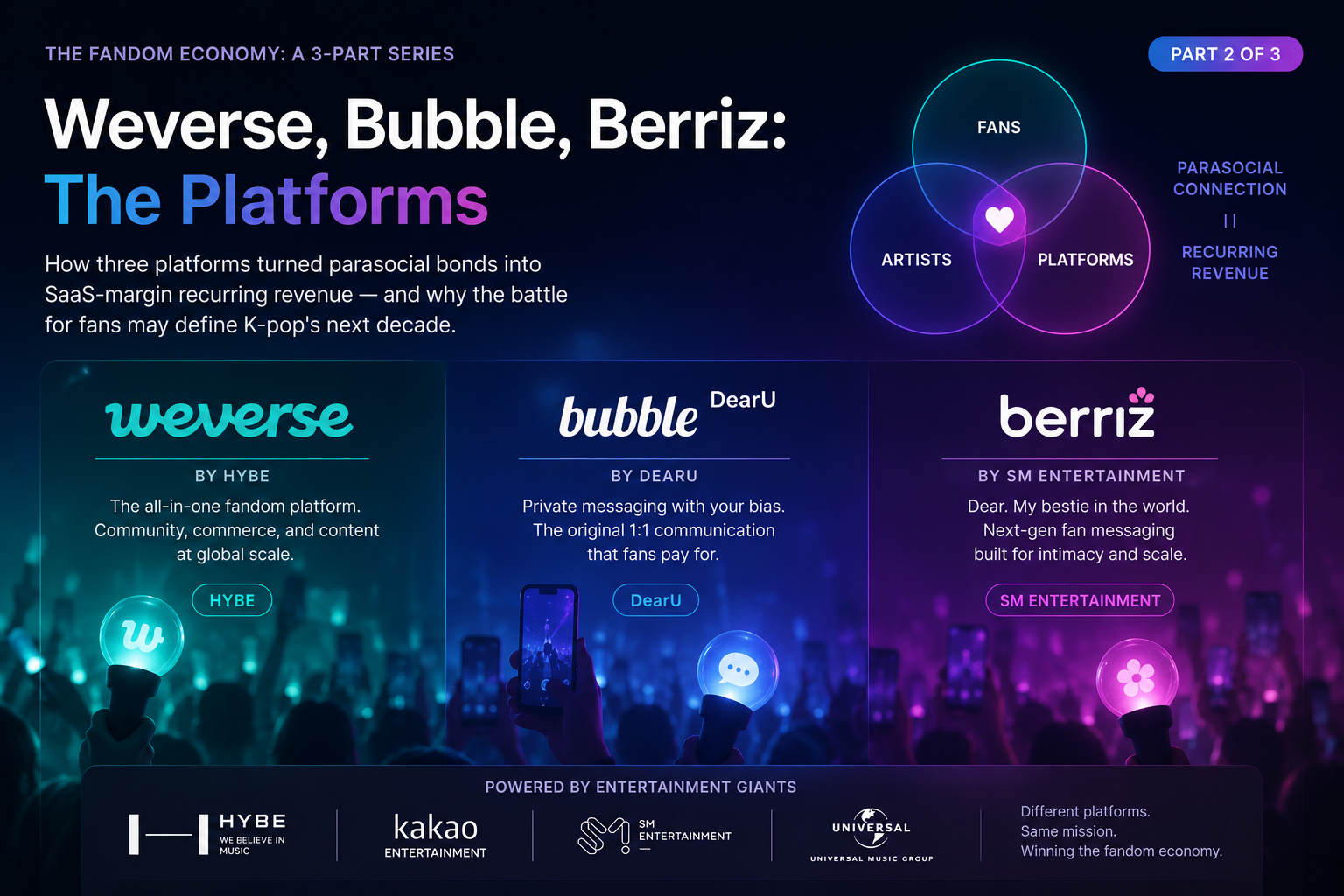

Weverse: The Super-App That Turned Profitable

When HYBE launched Weverse in 2019, the concept was ambitious to the point of appearing naive: a single platform hosting artist communities, livestreams, exclusive content, merchandise, subscriptions, and direct fan-to-artist messaging — all in one place, designed to own the entire fan relationship. Six years later, the concept has a name — the super-app — and it works.

In 2025, Weverse reached a peak of 12 million monthly active users — a milestone hit in June, when BTS’s full-group reunion triggered a 300%+ surge in new community followers in a single month. The BTS Weverse community became the first on the platform to surpass 30 million subscribers. Eighty-seven percent of users are based outside South Korea, making Weverse, in practical terms, a global product that happens to be Korean-owned.

The platform’s commerce arm tells a parallel story. 25.2 million products were sold through Weverse Shop in 2025, while digital product purchases more than doubled year-on-year. In Latin America — Weverse’s fastest-growing region — digital merchandise sales surged 715% year-on-year, coinciding with HYBE’s aggressive regional build-out through HYBE Latin America and new Spanish-language label DOCEMIL Music.

We aim to become a global entertainment lifestyle platform company based on music and technology — discovering a new universe and unlocking an immersive journey.

— HYBE, updated corporate vision statement, May 2026

Perhaps the most strategically significant Weverse development in 2025 was buried in HYBE’s Q3 earnings call: Weverse turned profitable on a cumulative annual basis. CEO Jae-sang Lee attributed the turnaround to growth in digital business lines — Weverse DM and Digital Membership — described as “independent profit models that continue to generate profit regardless of artist activities.” A platform that earns money even when the artists go quiet has escaped the fundamental volatility of the K-pop business cycle.

Weverse’s China expansion reinforces the same logic. Rather than building directly, HYBE partnered with QQ Music (Tencent) for Weverse DM access and opened Weverse Shop on Tmall (Alibaba), earning Tmall’s “2025 Supernova Brand” award in just five months. China’s two largest music streaming platforms together count around 171 million paying users — nearly double the US total — and HYBE now has distribution access without direct operational exposure.

Bubble: The Purest Business in the Industry

While Weverse attempts to be everything to everyone, DearU’s Bubble has built one of the most elegant business models in modern entertainment: charge fans approximately $4 per month per artist to receive messages that look like private 1:1 text conversations.

The interface mimics KakaoTalk, Korea’s dominant messaging app. The psychological effect is precisely calibrated — creating what researchers describe as the illusion of a personal relationship between idol and fan. The illusion is, in commercial terms, worth billions of won per quarter.

Physical merchandise carries manufacturing, warehousing, and shipping costs. Concerts require venues, crews, production. Even streaming involves complex royalty calculations. A Bubble message costs almost nothing to deliver — and fans pay per artist, per month, with no ceiling on how many artists they follow.

As of 2024, Bubble hosted 600 artists — covering roughly 51% of all active K-pop idols. Weverse covers 26%. The two platforms together account for nearly 80% of the idol-to-fan messaging market, according to University of British Columbia research. Academic scrutiny has followed commercial success: a 2025 study in Popular Music and Society noted that Bubble’s tiered revenue-sharing model creates structural pressure on artists to post continuously. NCT 127’s Jaehyun mentioned on Bubble that he felt he “should send at least four messages in a month.” Whether this is care, content creation, or compensated labor is a question the platform model deliberately leaves unanswered.

SM Entertainment raised its stake in DearU to 45.1% in early 2025, paying approximately $92 million for an additional 11.4%. The investment signals how seriously Kakao and SM view platform ownership as the core strategic asset — not the artists themselves, but the infrastructure through which artist relationships are monetized.

Berriz: The New Challenger Rewriting the Rules

On March 25, 2025, Kakao Entertainment launched Berriz — a global K-culture fan platform that arrives as neither a Weverse clone nor a Bubble successor, but as something more ambitious: a modular, IP-agnostic platform designed to unite fans of K-pop, K-drama, webtoons, musicals, and films under a single roof.

The strategic logic is clear. Kakao owns significant stakes in both Bubble (via SM Entertainment) and the broader K-content ecosystem. Berriz is the attempt to consolidate that footprint — extending the fan engagement model proven in K-pop across every form of Korean cultural IP simultaneously.

By mid-2025, CRAVITY, IVE, IU, MONSTA X, WOODZ, and multiple Starship and SM artists had opened communities on Berriz. The platform launched in 18 languages with full global payment and shipping infrastructure on day one — a signal that Kakao is not building for Korea. It is building for the same international audience that Weverse has already proven exists and will spend.

Just like berries that come in various shapes and sizes but become sweeter when gathered, Berriz will be a playground where global fandoms can communicate and enjoy K-culture together, transcending genres and boundaries.

— Kakao Entertainment, Berriz launch statement, March 2025

The Platform War: A Timeline

Initially BTS-centered. Rapidly expands to multiple HYBE artists and begins integrating commerce, live streaming, and exclusive content into a single ecosystem.

Pure SaaS model: fans pay per artist for intimate-feeling text messages. Interface mimics KakaoTalk. Spreads rapidly across SM and then cross-label artists. 600 idols by 2024.

Kakao’s SM acquisition creates strategic alignment between Bubble, SM’s artist roster, and Kakao’s technology stack. The foundation for Berriz begins to take shape.

UMG’s undisclosed Weverse investment signals that Western labels see the K-pop platform model as the future of superfan monetization globally. Ariana Grande and Dua Lipa join the platform.

Kakao launches Berriz with 18-language global infrastructure on day one. SM artists begin migrating. AI persona technology debuts. The market shifts from Weverse vs. Bubble to a genuine three-way competition.

Weverse achieves cumulative annual profitability. CEO confirms 30% annual growth in digital business lines. Platform revenue declared independent of artist activity cycles — the key milestone investors had been watching for.

With the BTS WORLD TOUR ‘ARIRANG’ underway across 82 shows in 34 cities, all three platforms compete for engagement share from history’s most commercially significant K-pop fanbase. MAU trajectories in 2026 will define the competitive landscape for years.

What This Means for the Rest of the Music Industry

Goldman Sachs now estimates the superfan platform opportunity at approximately $4.3 billion annually, identifying direct-to-fan platform infrastructure as one of the primary drivers of a projected $200 billion global music market by 2035. In January 2026, UMG Chairman Lucian Grainge told staff the company would “accelerate” its superfan efforts through “enhanced premium tiers” and partnerships with “emerging platforms.”

The emerging platforms he referenced are, mostly, K-pop’s creations. The model — recurring subscriptions, intimate messaging simulacra, gamified commerce, community identity — was not invented in Los Angeles or London. It was built in Seoul, tested on the most intense fanbases in modern entertainment history, and is now being licensed, invested in, and copied by every major player in global music.

- Weverse MAU12M peak (June 2025) · 11.2M by Q4 2025 · +15% rebound in January 2026 on BTS anticipation

- Weverse ProfitTurned cumulative profit in 2025 · Digital business growing 30% annually · Now >10% of total Weverse revenue

- Bubble~2M paid subscribers · 600 artists · DearU Q3 2025 revenue: ₩22.3B (~$17.4M per quarter)

- SM / DearUSM raised stake to 45.1% in 2025 for ~$92M · Platform ownership treated as core strategic IP

- Berriz LaunchMarch 25, 2025 · 18 languages · ~500 logistics hubs · AI personas · Berriz Shop live November 2025

- UMG InvestmentUndisclosed stake in Weverse (2024) · Ariana Grande, Dua Lipa now on platform · Western pivot confirmed

- China ExpansionWeverse DM live on QQ Music (Nov 2025) · Weverse Shop on Tmall · “Supernova Brand” award in 5 months

The deeper question — one the platforms have no financial incentive to answer — is what happens to fans inside these walled gardens over time. Every feature designed to deepen engagement also deepens dependency. Every subscription renewed signals that leaving would feel like loss. The platforms are not just monetizing fandom. They are, in the most precise sense of the phrase, managing it. That management is often experienced by fans as care. Whether it is something else — or both things at once — is what Part III is about.

Platform data cross-verified from: HYBE FY2025 and Q3 2025 Earnings Calls (Music Business Worldwide, Alpha Spread, Digital Music News, November 2025–February 2026); Weverse 2025 Fandom Trend Report (HYBE, February 2026); DearU Q3 2025 financial disclosures; SM Entertainment investor filings; Kakao Entertainment official Berriz communications (March, June, September, November 2025); Korea Herald (February 2025 Berriz/Weverse coverage); AllKPop (March 2025 Berriz beta launch); Popular Music and Society, “The Labor Process of Relational Labor” (Tandfonline, 2025); UBC platform coverage research cited in Seoulz; Goldman Sachs Music in the Air 2025 & 2026 editions (Music Business Worldwide); Outlook India Respawn Weverse vs. Bubble analysis (November 2025).