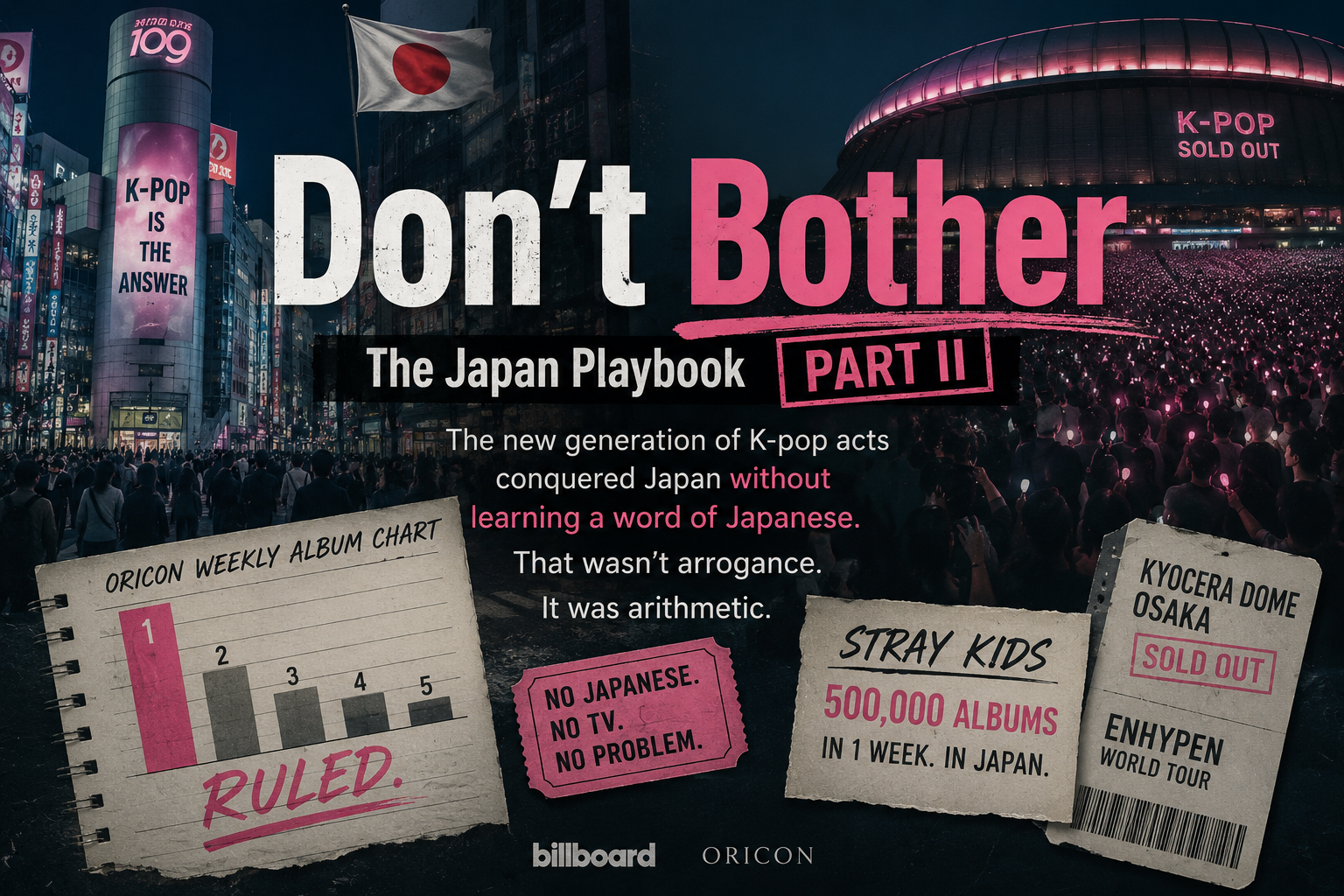

The new generation of K-pop acts conquered Japan without learning a word of Japanese. That wasn’t arrogance. It was arithmetic.

In June 2025, Stray Kids released a Japanese EP called Hollow. It sold 500,000 copies in its first week — the fastest first-week sales by any non-Japanese artist on the Oricon that year. The lyrics were in Japanese and English. The music was written by Bang Chan, Changbin, and Han — three Koreans who produce everything in Seoul. No Japanese songwriters. No Japanese label A&R direction. No Japanese television appearances in the months prior. No attempt to become, in any sense, Japanese.

BoA spent three years learning a language before she was allowed to release a single note. Stray Kids debuted their Japanese EP and headed to New York to headline Governors Ball.

Something changed. The question is what — and whether the change is as clean as it looks.

Chapter One

What the Pandemic Unlocked

The COVID-19 pandemic closed every concert venue in Japan for the better part of two years. It also, inadvertently, ran the largest test in K-pop history of what Japanese fans would do with nothing to attend.

The answer was: stream, buy albums, and spend their time on platforms that had no geographic borders. Between 2020 and 2022, Japanese K-pop consumption migrated to YouTube, TikTok, and Weverse at a pace that would have taken years under normal market conditions. The parasocial relationship that Japanese fans had historically built through television appearances and handshake events — the face-to-face contact rituals that had been central to the old playbook — was replaced by digital intimacy: Vlives, fan community posts, behind-the-scenes content released on global platforms simultaneously.

When the venues reopened, something had shifted. Japanese fans had spent two years engaging with K-pop acts on the same platforms, through the same content formats, as fans in Seoul, Los Angeles, and London. The localization layer — the Japanese-language singles, the NHK appearances, the domestic label infrastructure — had not been present during the pandemic, and the audience had not particularly noticed its absence. The music had crossed without it.

ENHYPEN’s trajectory illustrates this precisely. They debuted in November 2020 — in the middle of the pandemic — with no Japanese members, no Japanese debut strategy, and no ability to perform in Japan for over a year. By November 2022, they had sold more than one million albums on the Oricon in a single calendar year: the first fourth-generation K-pop group in history to do so. By January 2023, they were selling out Kyocera Dome in Osaka — the fastest K-pop group of their generation to headline a Japanese dome, achieved without a single member who spoke Japanese as a first language.

ENHYPEN Oricon album sales in 2022 alone — first 4th-gen K-pop group to achieve this in a single year

Stray Kids’ Hollow first-week sales (2025) — fastest non-Japanese artist debut week on Oricon that year

Share of Oricon 2025 year-end top 100 album spots taken by K-pop and K-pop affiliated acts

The Oricon 2025 year-end album chart confirmed what individual releases had been suggesting for several years. K-pop and K-pop affiliated acts — including NiziU, &TEAM, and NCT WISH — occupied nearly half of the top 100 spots. Stray Kids alone claimed five. SEVENTEEN, TXT, ENHYPEN, LE SSERAFIM, aespa, IVE, ATEEZ, BABYMONSTER — all present, all charting in Korean, most without any systematic localization strategy of the kind the first playbook demanded.

Japan had not lowered its standards. Japan had changed what it was looking for.

Chapter Two

The Arithmetic of Not Bothering

It would be easy — and wrong — to conclude that the new generation simply got lucky. That the pandemic created an opening, and they walked through it. The decision not to pursue full localization is not a passive absence of strategy. It is a deliberate calculation, and the math behind it is straightforward once you see it.

Under the old playbook, breaking Japan required committing roughly half a year’s activity to the Japanese market: recording Japanese-language albums, filming Japanese-specific content, appearing on domestic television, building relationships with Japanese media. For BoA in 2001, that was an acceptable trade — Japan was K-pop’s primary international revenue source, and there was nowhere else for the money to go. For a group operating in 2024, the same six months spent on Japan-specific localization means six months not spent on a Billboard 200 promotional cycle, not spent on a North American tour, not spent on the global streaming platforms that now determine an act’s commercial ceiling.

KpopWave Editorial

The data makes this visible. In Q1 2026, South Korea’s music album exports hit a record $120 million — up 159% year-over-year, the first time a single quarter had exceeded $100 million. The United States accounted for 28% of that total, edging out Japan for the first time in nearly a decade. Japan remained the largest single-country market in 2025 at $80.6 million annually — but the US is closing fast, and the trajectory is unambiguous.

For a K-pop label in 2026, the strategic logic is not “ignore Japan.” It is “stop treating Japan as the only game worth playing.” The acts that are winning in Japan right now — Stray Kids, SEVENTEEN, ENHYPEN — are also winning in the United States, Europe, and Southeast Asia. Their Japan strategy is a subset of their global strategy, not a separate operation requiring its own language, its own album catalog, and its own television relationships.

They still release Japanese-language music. Stray Kids’ Hollow is in Japanese. ENHYPEN’s Sadame is in Japanese. The difference is that the Japanese-language output is now produced by the same Korean creative teams, through the same Seoul-based production infrastructure, as everything else. The localization is linguistic, not cultural. The music does not try to become Japanese. It arrives as K-pop, in Japanese, and the Japanese audience has decided that is sufficient.

Chapter Three

The Basecamp

In November 2025, Pollstar published its Asia Focus chart for top touring artists. SEVENTEEN placed second, behind only Coldplay. ENHYPEN placed third. J-Hope placed fifth. TXT eighth. Hybe alone had multiple acts in the top ten — the only company to do so.

The Japan component of this touring dominance is not incidental. Tokyo, Osaka, Fukuoka, Nagoya — four major dome cities, each capable of hosting 50,000 to 55,000 people, each within domestic flight distance of the others. A single Japanese dome run of four cities, four nights each, produces 800,000 to 900,000 ticket transactions in roughly ten days of activity. The logistics cost a fraction of an equivalent North American stadium tour. The margin per ticket, after venue fees and production costs, runs significantly higher. Japan is not where K-pop builds its cultural profile anymore. It is where K-pop makes a large portion of its actual money.

Venue density: Tokyo Dome (55,000), Kyocera Dome Osaka (55,000), Fukuoka PayPay Dome (53,000), Vantelin Dome Nagoya (49,000) — four 50,000+ venues within domestic flight range. No other country offers this concentration at this scale.

Logistics cost: A four-dome Japan run costs a fraction of a comparable North American stadium tour. No transatlantic freight, no visa logistics for 100+ crew members, no multi-timezone production coordination.

Fan spending: Japanese concert attendees average significantly higher per-show merchandise spend than any other K-pop market. The ¥30 million (~$200K) average merchandise revenue per concert in Japan (2023) is a baseline, not a ceiling for major acts.

Multi-stanning culture: Japanese fans are more likely than any other market to follow multiple K-pop acts simultaneously — meaning the audience base is not zeroed out when a single group is on hiatus or in the military.

This is what “Japan as basecamp” actually means in practice. The album chart supremacy that BoA and TVXQ built through years of cultural assimilation has been converted, by the current generation, into a reliable touring infrastructure that funds global expansion. Japan is not where K-pop proves itself anymore. Japan is where K-pop finances itself.

The shift from prestige market to profit center happened gradually, and then all at once. The pandemic accelerated it. The globalization of streaming completed it. And the numbers from Q1 2026 — the US overtaking Japan in album exports for the first time — mark its formal arrival.

Japan did not lose. But it changed roles. And the K-pop industry, with its characteristic efficiency, noticed and adjusted before most observers had finished processing what was happening.

I want to be careful about the conclusion this series appears to be leading toward — the triumphalist reading, in which K-pop simply got smarter, stopped bothering with localization, and is now winning everywhere simultaneously. That reading is too clean.

Japan is still the second-largest music market in the world. It still generates $80 million a year in K-pop album exports. It still hosts the dome infrastructure that funds much of the industry’s global touring. The fact that the United States is now buying more K-pop albums quarterly does not diminish Japan’s structural importance — it reflects the extraordinary speed at which American fans have adopted the purchasing behaviors that Japanese fans spent a decade developing. America did not invent the K-pop album as collectible artifact. Japan did. America is now running the same playbook.

What I find genuinely unsettling about the current moment is not the shift in album market share. It is what that shift might imply about Japan’s long-term position in the K-pop ecosystem. Multi-stanning culture, dome touring revenue, and decades of fan loyalty have made Japan the most stable K-pop market in the world. Stable, in industry terms, often means mature. And mature, in industry terms, often means the growth ceiling has arrived.

BoA quit school at fifteen to learn a language. The question worth asking now is whether Japan, which demanded that sacrifice and rewarded it so handsomely for twenty years, is now simply a very well-maintained machine that no longer requires anyone to change themselves to operate it. That is an achievement. It is also, perhaps, the most polite way the music industry has ever described a market becoming less interesting than it used to be.

The basecamp metaphor is accurate. Basecamps, by definition, are where you sleep before the real climb. Nobody stays.